Overview

The Social Security Administration (SSA), Centers for Medicare & Medicaid Services (CMS), and Internal Revenue Service (IRS) have announced new benefit and tax parameters effective January 1, 2026. This memo summarizes those key changes and compares them with 2025 values currently in effect.

All data reflect official SSA, CMS, and IRS releases as of November 2025.

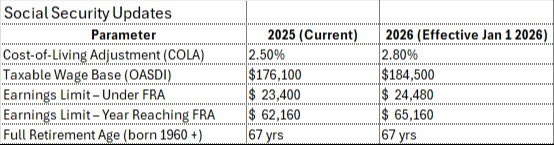

The earnings limit determines how much work income can be earned before benefits are temporarily reduced for those claiming before full retirement age.

--------------------------------------------

Hold-Harmless Rule:

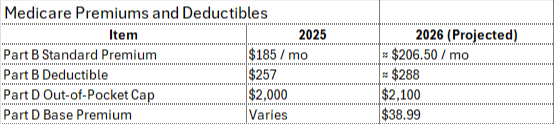

Most beneficiaries are protected from a reduction in their Social Security benefit if the Part B premium increase exceeds their COLA.

This protection does not apply to new Part B enrollees or those subject to IRMAA surcharges.

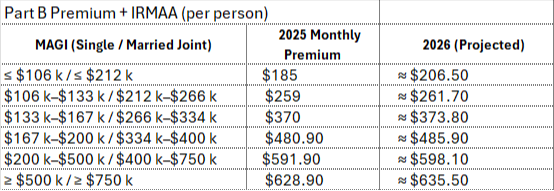

High-Income Surcharges (IRMAA)

Beneficiaries with higher modified adjusted gross income (MAGI) from two years earlier pay surcharges on Medicare Parts B and D.

For 2026, SSA will use 2024 tax-return income.

Important: IRMAA surcharges are per person, but thresholds for married couples filing jointly are based on combined household income.

If joint MAGI exceeds a threshold, each spouse pays the corresponding surcharge individually.

--------------------------------------------

Appealing an IRMAA Determination

If income declined due to a life-changing event, you may request review using SSA Form 44.

Qualifying events include:

• Retirement or reduced work hours

• Marriage or divorce

• Death of a spouse

• Loss of pension or property income

SSA may recalculate IRMAA based on current income rather than the two-year-old return.

Filing Status Note

Filing Married Filing Separately almost never reduces IRMAA and generally increases it.

MFS filers face higher premiums unless they lived apart all year under SSA rules.

Filing jointly is typically more favorable.

Planning Implication:

Manage IRMAA through income-timing, Roth conversions, and Form 44 appeals, not filing-status changes.

--------------------------------------------

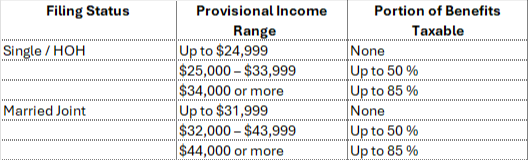

Taxation of Social Security Benefits

Benefits may be taxable depending on Provisional Income = AGI + Nontaxable Interest + ½ of Benefits Received.

Thresholds are not indexed for inflation, so more retirees become taxable over time.

State treatment varies; Pennsylvania exempts Social Security benefits.

Planning Implication: Coordinate distributions and conversions to manage provisional income.

--------------------------------------------

Additional Tax Updates for 2026

- Standard Deduction Increase:

For 2026, the standard deduction is projected at approximately $16,300 (single) and $32,600 (married joint).

Taxpayers age 65 or older qualify for an additional $2,050 (single) or $1,650 (per spouse if joint). - New Senior Bonus Deduction:

Under the One Big Beautiful Bill Act (2025), individuals age 65 or older may claim an extra $6,000 deduction per person ($12,000 per couple if both qualify).

This benefit phases out for higher-income taxpayers beginning around $75,000 MAGI (single) and $150,000 MAGI (joint).

The deduction is available for tax years 2025 through 2028. - Example: Married Filing Joint both over age 65 standard deduction for 2025 will be $47,500. Single over age 65 standard deduction will be $24,150. (Assumes full eligibility and no phase-out of the bonus deduction due to high income.)

- Bracket and Credit Phase-Out Adjustments:

Income limits for federal tax brackets, IRA and Roth IRA eligibility, and the Qualified Business Income deduction are rising modestly for 2026, improving after-tax outcomes for many retirees.

-------------------------------------------

Planning Highlights for 2026

- COLA + 2.8 % helps offset inflation, though purchasing power may still lag.

• Higher earnings limits reduce benefit withholding before FRA.

• Roth conversion timing and distribution planning help control IRMAA and tax exposure.

• Include new deduction and premium changes in cash-flow forecasts.

• Crosswalk continues to monitor SSA, CMS, and IRS policy updates.

As always, if you have any questions or concerns about how these 2026 changes may affect your Social Security benefits, Medicare premiums, or tax planning, we welcome the opportunity to discuss them with you.